Germany confirms its position as the world’s second-largest importer of technologies for the printing, graphic and converting machinery industry, second only to the United States.

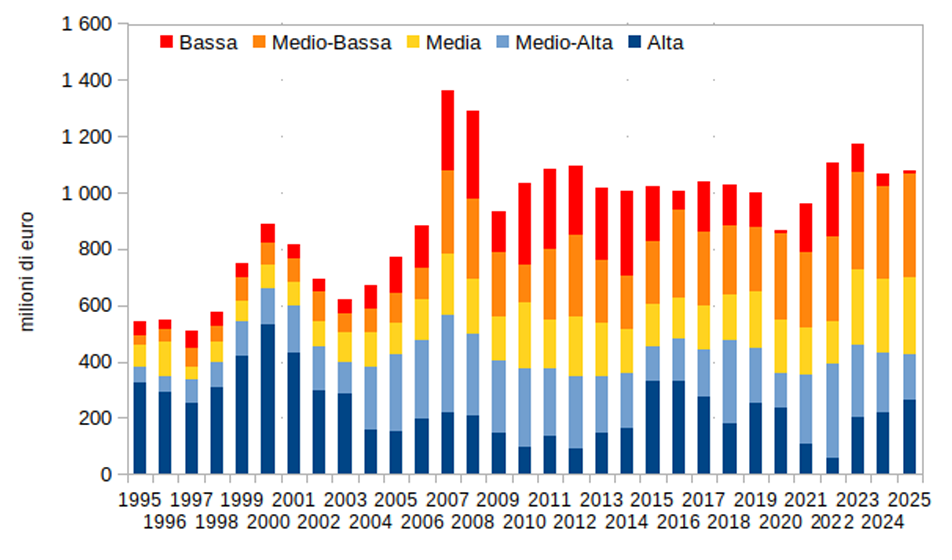

By the end of 2025, imports into the German market remained above €1 billion. This level is broadly in line with the last decade, though still below the peak reached in 2007-2008, when values approached €1.3 billion. The qualitative composition of German imports of printing and converting technologies shows, however, a slight preference for lower price segments. Overall, in 2025 (according to ExportPlanning analyses), imports in the High and Upper-Middle price ranges accounted for just under 40% of total market imports. Conversely, lower price segments represented around one third of total import flows.

According to ExportPlanning forecasts, in the 2026-2029 scenario, German imports of printing and converting machinery are expected to grow at a moderately positive average annual rate in euro terms (CAGR: +2%), reaching over €1,150 million (an increase of more than €87 million compared to 2025). However, forecasts show differentiated trends across segments, with positive dynamics for printing machinery (CAGR: +4.2%), papermanufacturing machinery (CAGR: +1.4%) and converting machinery (CAGR: +1.1%), while negative trends are expected for bookbinding machinery and machines and materials for pre-press/form preparation.

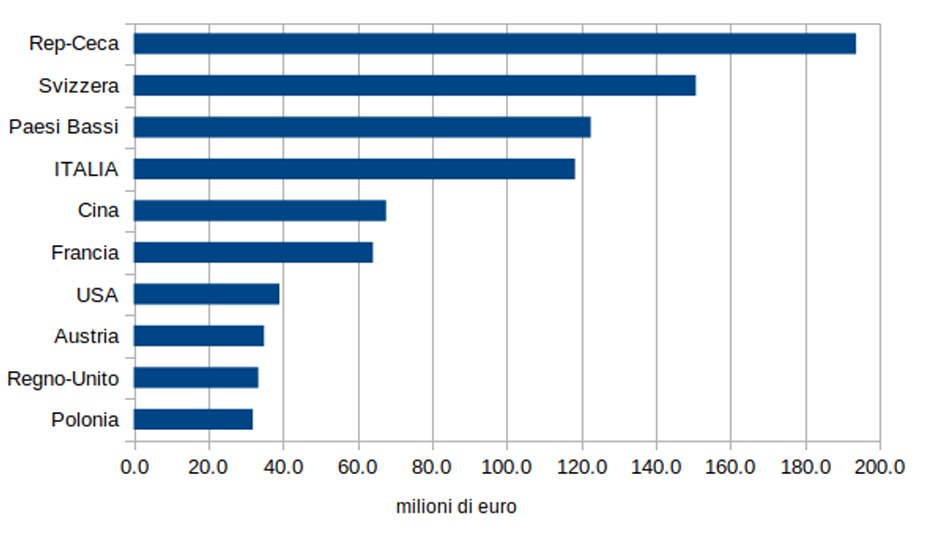

Czech Republic leading supplier in 2025, Italy ranks 4th

Czech Republic was the leading supplier to the German market in 2025, with a 18% market share. Italy ranked fourth among supplier countries, with an export value of €118.4 million in 2025 (11% share), ranking right behind Switzerland and the Netherlands. According to ExportPlanning forecasts, in the 2026-2029 scenario Italian exports to Germany are expected to show moderate growth, with an average annual growth rate (CAGR) of +1.2% in euro terms, reaching €124.3 million by the end of the period.

Composition of German imports by segment

Breaking down German imports of printing, paper and converting machinery by segment, in 2025 the highest import values were recorded for printing machinery (€428 million) and converting machinery (€372 million), followed – at quite a distance – by paper-manufacturing machinery (€117 million), machines and materials for prepress/ form preparation (€90 million), and bookbinding machinery (€58 million). In the 2026-2029 scenario, the largest contributions to growth are expected to come from printing machinery (+€77.1 million) and, to a much lesser extent, converting machinery (+€17.3 million).

Italian exports to the German market by segment

In 2025, Italian exports to Germany recorded the highest values in converting machinery (€61.4 million) and printing machinery (€39.8 million), while all other segments remained below the €10 million figure. Forecasts for the 2026-2029 period see Italian exports expected to receive the strongest positive contributions from printing machinery (+€4.3 million, driven by a strong acceleration already expected in 2026) and converting machinery (+€3.3 million, corresponding to a CAGR of +1.3%), while other segments are expected to show comparatively weak dynamics.

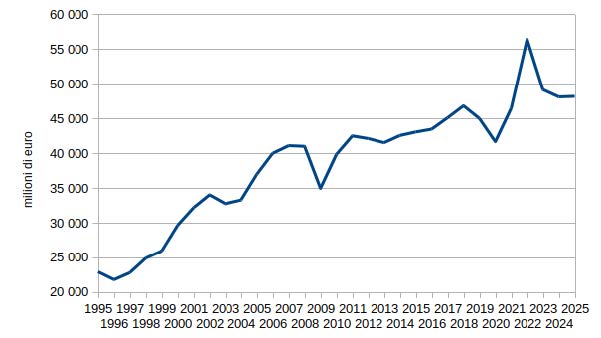

German production in the printingpaper- converting value chain

German production in this sector is estimated at €48.2 billion (2025 estimates), making the country the third-largest global producer in the value chain (behind China and the United States). Over the period analysed, German production showed a phase of sustained and prolonged growth up to the 2008-2009 Great Recession (CAGR 2007/1995: +5%), followed by a return to growth – albeit at more moderate rates – in the subsequent period (CAGR 2025/2009: +2%).

The largest values within the German printing and paper converting chain are strong in Flexible Packaging (€16 billion estimated for 2025, making Germany the world’s third-largest producer), Packaging Paper and other paper converting products (€9 billion, ranking second worldwide), and Graphic Paper (€5.1 billion, making Germany the leading producer globally). The country also holds significant positions in Graphic and Publishing Products (2nd worldwide, with a value of €4.8 billion), Finished Tissue Products (3rd globally, worth €4.5 billion), Paper Converting Products (2nd worldwide, with a value of €2.6 billion), Paper and Board Packaging (2nd globally, worth €3.2 billion), and Bags/Shopping Bags (2nd worldwide, with a value of €2 billion).

{kind=link}